search

date/time

Mon, 1:00PM

overcast clouds

24.1°C

ESE 10mph

overcast clouds

24.1°C

ESE 10mph

| Sunrise | 3:32AM |

| Sunset | 8:40PM |  |

P.ublished 1st April 2026

business

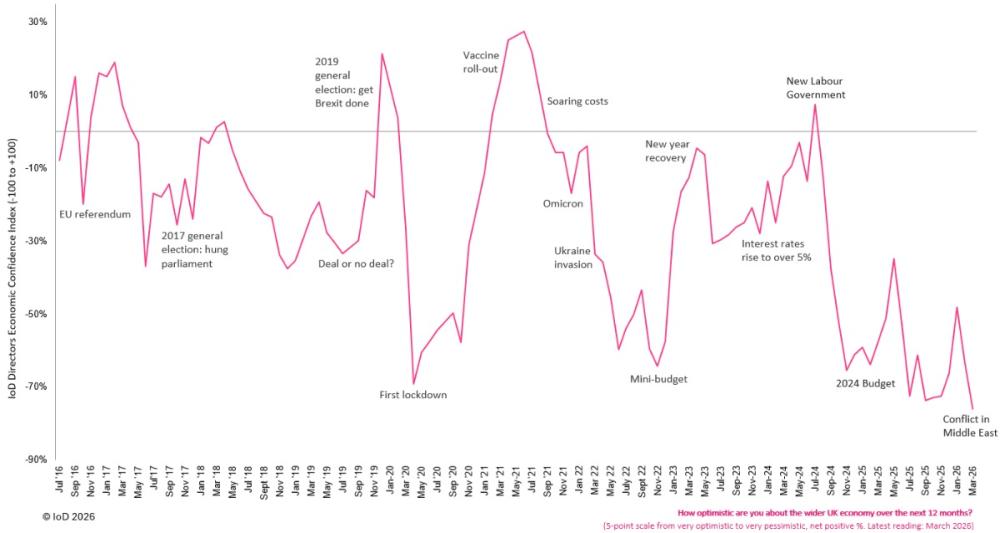

IoD: Middle East Conflict Drives Economic Confidence To New Record Low

The IoD Directors’ Economic Confidence Index, which measures business leader optimism over prospects for the UK economy, fell to its lowest ever reading of -76 in March 2026, from -63 in February.

Business leader confidence in their own organisations also fell, to -2 in March from +1 in February.

Cost expectations rose to +88 in March from +84 in February, the second highest reading on record (+89 in Sept 2025)

Investment intentions fell to -13 from -6 (investment intentions have been net negative every month since August 2024)

Revenue expectations dipped to +13 from +15

Export expectations dipped to +2 from +5

Wage expectations rose to +47 from +45

Headcount expectations rose to ±0 from -11

71% are concerned about geopolitical tensions affecting investment, markets or business partners

69% are concerned about energy price volatility

60% are concerned about cyber-attacks or technical sabotage

58% are concerned about supply chain disruption

In terms of the factors driving directors outlook for costs over the year ahead, the largest factors were labour (including employment taxes) listed by 71%, followed by supply chain inflation (51%) and energy (39%).

When asked about the conflict in the Middle East, 59% of business leaders stated that it has had a negative impact on their organisation so far, with around a third saying the impact was neutral so far.

.jpg)

Anna Leach

The outbreak of conflict in the Middle East has driven down the confidence of business leaders to a new record low. Manufacturers are at the sharp end, with 69% reporting a negative impact so far, compared to a cross-sector average of 59%. Impacts being reported include sharp increases in fuel and shipping costs, rising material prices – such as petrochemicals – and delivery delays. Across all sectors, the general increase in uncertainty is once again delaying decision-making, as many wait to see how the conflict evolves. Financial conditions are reported to have tightened, with investors pulling out of deals. Some offsetting positivity is reported in the renewables sector, where enquiries have understandably increased. But the overall effect is that economic activity has weakened from its already subdued level, while inflationary pressures once again are building.

More muted changes in underlying data, such as investment intentions and revenue expectations mirror the likewise moderate changes in oil and gas prices despite the unprecedented closure of the Strait of Hormuz. The longer and more severe the hit to global energy supplies, the harder businesses and the broader economy will be impacted.

The government is right to be alert to the risks of another cost shock to the economy, and has been agile in giving vital support to households exposed to heating oil costs. But it should avoid framing price increases as profiteering when many businesses are facing genuine and significant cost pressures from energy, logistics and supply chain disruption.

Full Results

591 responses from across the UK, conducted between 13-30 March 2026. 11% ran large businesses (250+ people), 22% medium (50-249), 25% small (10-49 people), 28% micro (2-9 people) and 14% sole trader and self-employed business entities (0-1 people).

How optimistic are you about both the wider UK economy and also your organisation over the next 12 months?

| Very optimistic | Quite optimistic | Neither optimistic nor pessimistic | Quite pessimistic | Very pessimistic | Don't know | |

| Wider UK economy | 0.3% | 4.1% | 14.9% | 50.3% | 30.3% | 0.2% |

| Your (primary) organisation | 2.5% | 26.1% | 39.9% | 25.2% | 5.8% | 0.5% |

Comparing the next 12 months with the last 12 months, what do you believe the outlook for your organisation will be in terms of:

| Much higher | Somewhat higher | No change | Somewhat lower | Much lower | N/A | Don't know | |

| Business investment | 3.7% | 20.3% | 36.0% | 22.5% | 14.4% | 2.5% | 0.5% |

| Costs | 20.6% | 68.9% | 7.4% | 1.0% | 0.7% | 0.7% | 0.7% |

| Exports | 1.9% | 13.0% | 27.6% | 8.5% | 4.2% | 43.7% | 1.2% |

| Headcount | 1.9% | 21.7% | 50.1% | 19.6% | 4.2% | 2.0% | 0.5% |

| Revenue | 5.1% | 37.9% | 25.4% | 24.4% | 5.6% | 1.0% | 0.7% |

| Wages | 4.4% | 51.9% | 30.8% | 7.1% | 2.4% | 2.5% | 0.8% |

How concerned are you about the following economic security risks? Please tick all that apply.

| Geopolitical tensions affecting investment, markets, or business partners | 70.6% |

| Energy price volatility | 68.5% |

| Cyber-attacks or technical sabotage | 60.2% |

| Supply chain disruption | 58.4% |

| Trade barrier shifts e.g. tariffs or sanctions | 36.0% |

| Economic coercion | 23.4% |

| Foreign investment, ownership or partnerships | 19.5% |

| Dependence on a small number of overseas suppliers for critical inputs | 19.1% |

| Intellectual Property theft | 16.4% |

| Economic crime or illicit finance | 13.9% |

| Climate-related disruptions affecting operations or supply chains | 12.9% |

| Other | 6.1% |

| None | 1.4% |

| Don't know | 0.2% |

To what extent has the conflict in the Middle East had an impact on your organisation so far?

| Strong positive impact | 2.4% |

| Slight positive impact | 2.9% |

| Neutral | 33.3% |

| Slight negative impact | 45.9% |

| Strong negative impact | 13.2% |

| Don't know | 2.4% |